View:

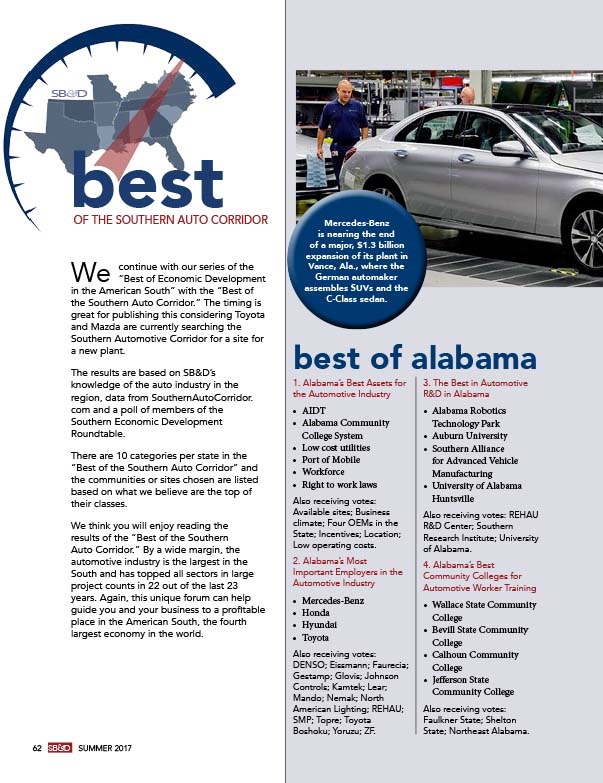

Best of The Southern Auto Corridor

For real-time news on business, politics and economic development in the South, go to www.RandleReport.com. For all projects announced in the South, go to www.SB-D.com. For more information on the automotive industry in the South, go to www.SouthernAutoCorridor.com.

Kamtek opens expanded Birmingham plant

BMW celebrates 4 millionth vehicle made in South Carolina

Brazilian manufacturer to open first U.S. facility in rural Virginia

Vehicle glass manufacturer expands in Virginia

German auto supplier launching new operations in South Carolina

Another megasite planned for the American South

Auto supplier expanding in West Georgia

Has Alabama’s ROI in the automotive sector paid off?

Bus manufacturer expands Alabama plant

Aluminum manufacturer investing $110 million in Tennessee

Japanese auto parts supplier to build new plant in Tennessee

Alabama lands truck manufacturer

Racing and auto parts manufacturer adding ops in Franklin, Ky.

Hino Motors Manufacturing expands in West Virginia

Billion-dollar expansion for Mercedes-Benz in Alabama

Toyota investing $374 million at five U.S. plants

Auto supplier JTEKT opens new plant in Tennessee

Volvo will boost U.S. investment to $1.1 billion

Bilstein Cold Rolled Steel opens new facility in Bowling Green, Ky.

Nokian Tires breaks ground on $360 million facility in Tennessee

Borgwarner expanding in South Carolina

BorgWarner investing $20 million, adding 75 jobs in Mississippi

Metalsa Structural Products expands in Owensboro, Ky.

Thrace-Linq expands South Carolina plant

Chinese automakers plan U.S. factory

For real-time news on business, politics and economic development in the South, go to www.RandleReport.com. For all projects announced in the South, go to www.SB-D.com. For more information on the automotive industry in the South, go to www.SouthernAutoCorridor.com.

Kamtek opens expanded Birmingham plant

Kamtek, a division of Magna, opened the $60 million, 150,000-square-foot expansion of its automotive parts facility in Birmingham, Ala., in the summer quarter. The project will add 100 workers to the plant, which currently houses 850. The company makes aluminum castings for vehicles made by Mercedes-Benz, Volkswagen and Nissan.

BMW celebrates 4 millionth vehicle made in South Carolina

In the summer quarter, BMW celebrated the 4 millionth vehicle made at its plant in Greer, S.C. The plant began making vehicles at the plant in 1994.

Brazilian manufacturer to open first U.S. facility in rural Virginia

Koinonia, a manufacturer of foam and tape solutions for the automotive, marine and heavy equipment industries, is investing almost $5 million in a new plant in Pulaski County, Va. The plant will house 40 workers.

Vehicle glass manufacturer expands in Virginia

Oran Safety Glass, a maker of specialty glass used in the manufacture of buses, military vehicles and trains, is expanding its Greensville, Va., operation. The $4.4 million project will create 55 jobs and retain 75.

German auto supplier launching new operations in South Carolina

Isringhausen, a seating systems manufacturer, is launching new operations in Charleston County in Ladson, S.C. The company, which has 50 plants in 20 countries, will make seats and assemblies for the Mercedez-Benz Vans Sprinter model.

Another megasite planned for the American South

The South is certainly not in short supply of large industrial sites of 1,000 acres or more. Add another one to the mix, this one in Chesterfield County, Va. Right before the recession a master-planned community in Chesterfield that would have contained 2,449 single-family homes, 1,331 condos, 908 apartments and 470,000 square feet of commercial space was announced. Called Branner Station, the plan was nixed by the Great Recession. Now Chesterfield wants to develop the wooded property as a 1,700-acre megasite for a large user such an an automotive or aerospace plant. The site is near Interstate 95 and the Port of Richmond.

Auto supplier expanding in West Georgia

Hyundai Dymos is adding 150 jobs to its workforce of 350 in West Point, Ga., near the Kia assembly plant. The $9.5 million expansion will add car seat capacity. The company makes seats for both the Kia plant and Hyundai’s plant in nearby Montgomery, Ala.

Has Alabama’s ROI in the automotive sector paid off?

By Michael Randle

In September 1993, the state of Alabama was highly criticized for the $253 million incentive package it gave Mercedes-Benz to locate its first plant in the U.S. in Tuscaloosa County. Alabama offered a package that was double that of what South Carolina had given to locate BMW just a year earlier.

Then in 1999, Honda announced it, too, would build a plant in Alabama. . .this one in East Alabama. That initial package totaled $158 million. In 2002, Hyundai followed Honda with its own plant announcement in Montgomery. Alabama’s initial package to Hyundai was $234 million.

Counting second and third incentive packages for expansions, the total Alabama has given out in site prep, training, tax breaks and other incentives is less than $1 billion for the three automakers.

So, to more easily understand the return on investment, let’s eliminate anything Alabama could have received from the three automakers, including the attraction of more than 250 suppliers to the state, tax generation, multipliers, spin-off jobs and anything else that’s difficult to calculate. Let’s just add up the payroll of the three automakers just at their facilities since they began operating. Why payroll? It’s something everyone understands because most of us are on a payroll.

SB&D’s estimated payroll since Mercedes, Honda and Hyundai have been operating their plants in Alabama is right at $12 billion. That’s a 12-fold ROI and that just counts payroll at the three assembly plants. What’s more, those plants will be operating 50 years from today.

Bus manufacturer expands Alabama plant

Canada-based New Flyer, North America’s largest transit bus manufacturer, is expanding its plant in Anniston, Ala. The company is investing $25 million and adding 40 new jobs.

Aluminum manufacturer investing $110 million in Tennessee

Sweden-based Granges, a manufacturer of aluminum products, is investing $110 million in its plant in Huntingdon, Tenn. to expand capacity from 160 to 200 metric kilotons per year. The company makes light gauge foil and automotive heat exchanger products. The deal will create 100 new jobs.

Japanese auto parts supplier to build new plant in Tennessee

Miyake Forging announced in the summer it will build a 45,000-square-foot facility in Hawkins County, Tenn. The bearings manufacturer will invest $13.7 million in the plant that will house 60 workers.

Alabama lands truck manufacturer

Autocar, a manufacturer of a wide variety of trucks, announced in the summer plans to build a $120 million facility near Birmingham, Ala. The plant will assemble heavy-duty, cab-over-engine trucks. The deal will create 746 jobs.

Racing and auto parts manufacturer adding ops in Franklin, Ky.

Holley Performance Products, a top name in automotive racing and performance parts manufacturing, will establish a $9.15 million facility in Franklin, creating 30 full-time jobs.

Hino Motors Manufacturing expands in West Virginia

Japan-based truck maker Hino Motors Manufacturing will invest $100 million to relocate its assembly plant from Williamstown to Mineral Wells, W.Va. The company plans to purchase the former Cold Water Creek distribution center and convert it into a 1-million-square-foot truck assembly plant in Mineral Wells, close to its current plant. The new plant will also house cab assembly, an operation currently conducted in Japan. The company’s president, Takashi Ono, said the move was necessary for growth and the addition of 250 employees.

Billion-dollar expansion for Mercedes-Benz in Alabama

Mercedes is spending $1 billion to make electric SUVs at its Tuscaloosa plant, as well as building a 1 million-square-foot battery plant, a logistics center and after-sales North American hub. Thanks to an earlier investment of $1.3 billion announced in 2015, the Tuscaloosa plant is currently being expanded to prepare for the production of the next-generation SUV including plug-in hybrid models. The expansion will create more than 600 jobs.

Toyota investing $374 million at five U.S. plants

Toyota Motor Corp announced a $374 million investment at five U.S. plants to support production of its first American-made hybrid powertrain. The upgrades at Toyota’s factories in Alabama, Kentucky, Missouri, Tennessee and West Virginia are part of a previously announced $10 billion in U.S. spending by the Japanese automaker.

Auto supplier JTEKT opens new plant in Tennessee

JTEKT recently held a grand opening for its new plant in Vonore, Tenn. The plant means 100 new hires for the Japan-based manufacturer of driveline and steering components.

Volvo will boost U.S. investment to $1.1 billion

Even before the first vehicle rolls off the line at Volvo Cars’ new factory in South Carolina, the Swedish automaker has nearly doubled its investment to $1 billion and promised to build a second vehicle — the next-Generation XC90 — at the site. Volvo says it will spend an additional $520 million and add nearly 2,000 more jobs, bringing total employment to nearly 4,000, to its plant under construction in Berkeley County, 30 miles northwest of the port in Charleston.

Bilstein Cold Rolled Steel opens new facility in Bowling Green, Ky.

A family-owned German manufacturer is beginning operations at its facility in Bowling Green. Bilstein Cold Rolled Steel expects to employ about 110 people at its plant, which broke ground in 2015. The company creates thin pieces of steel for a variety of industries.

Nokian Tires breaks ground on $360 million facility in Tennessee

Nokian Tires recently broke ground on its $360 million manufacturing facility in Dayton, Tenn., Rhea County’s largest foreign direct investment to date.

Borgwarner expanding in South Carolina

A manufacturer of automotive powertrains is expanding its facility in the Upstate. BorgWarner is investing $71.9 million and creating more than 160 new jobs at its plant in Oconee County, the third expansion to its Seneca plant since 2013.

BorgWarner investing $20 million, adding 75 jobs in Mississippi

Automotive supplier BorgWarner is investing $20 million and adding about 75 jobs during the next two years at its Water Valley facility. BorgWarner bills itself as a leader in clean technology solutions for combustion, hybrid and electric vehicles.

Metalsa Structural Products expands in Owensboro, Ky.

Automotive frame manufacturer Metalsa Structural Products will be adding 113 jobs at its Owensboro facility as part of a $36.5 million expansion. Metalsa plans to produce a new line of stamped and welded components.

Thrace-Linq expands South Carolina plant

Thrace-LINQ, a global supplier of fabrics for the textile industry and member of the Greece-based Thrace Group, will invest $9 million to expand its operations center in Dorchester County, S.C. The company will be adding a new production line and upgrading existing equipment to produce nonwoven fabrics used in a variety of applications, including geosynthetics, automotive, construction and floor covering.

Chinese automakers plan U.S. factory

Wei Jianjun, chairman of Great Wall Motor Co, said that the carmaker intends to set up a manufacturing presence in the US, in cooperation with two other Chinese car producers. “The three Chinese auto companies may test the waters by building a factory together,” Wei was quoted as saying, without naming the two other firms. A Beijing-based media group reports that three other Chinese automakers — Geely, Guangzhou and Chery – have all previously announced plans to enter the U.S. market. Geely and Guanzhou both said they were unaware of the plans, while Chery declined to comment. Wei described the move as “brand-building to sell cars in the US.” It also comes under a Trump administration eager to announce new manufacturing jobs.

For real-time news on business, politics and economic development in the South, go to www.RandleReport.com. For all projects announced in the South, go to www.SB-D.com. For more information on the automotive industry in the South, go to www.SouthernAutoCorridor.com.

Kentucky has become the center of aluminum manufacturing for the automotive industry

In the spring quarter, Braidy Industries announced it will build a $1.3 billion aluminum mill in Greenup County in Eastern Kentucky. The plant will produce aluminum sheet and plate for automotive plants in the South and Midwest. The deal will create 550 jobs. With Ford using more aluminum in its vehicles that are built in Louisville, the plant is needed. Also, Toyota is undergoing a $1.3 billion expansion of its plant in Georgetown, Ky., part of which is to accommodate more aluminum parts in its vehicles assembled there. The move convinced Logan Aluminum, which for decades has made aluminum cans in Logan County, Ky., to invest $248 million in the plant to produce aluminum parts for cars and trucks.

South Carolina automotive plant moving to Mexico

Kongsberg Automotive will close its plant in Easley early next year and eliminate nearly 100 jobs. The plant makes parts for large trucks and buses.

Who’s in the running for Toyota-Mazda plant?

According to the Wall Street Journal, 11 states — Alabama, Florida, Kentucky, Illinois, Indiana, Iowa, Michigan, Mississippi, North Carolina, South Carolina and Texas — are being considered for a $1.6 billion auto manufacturing plant planned by Toyota and Mazda.

Freightliner to open $27 million logistics center in North Carolina

Rowan County’s huge Freightliner plant, owned by Portland, Oregon-based Daimler Trucks North America, will get a new $27 million logistics center and add more than a dozen new jobs to the 1,400 employees already working there. The idea is to consolidate existing warehouses and pave the way for adding more robot vehicles to the production line.

Toyota Motor North America expands Plano, Texas operations hub

Toyota Motor North America will form a new group focused on new technologies for its Toyota and Lexus vehicles. Called Connected Technologies, the group will employ approximately 100 positions and will include members from Toyota’s existing teams working on connected vehicles, information systems, and research and development.

Sentury to build North American HQ and tire plant in Georgia

Sentury Tire’s Georgia-based North American headquarters and manufacturing plant will sprawl across 1.5 million square feet, according to a filing made with the state. Last September, China-based Sentury Tire confirmed plans for a $530 million investment in LaGrange to make tires for cars and aircraft, including the landing gear tire for the Boeing 737. The first phase will employ 1,000 and include R&D and distribution centers.

Parts supplier to establish new operation in South Carolina

Germany-based Frimo Group subsidiary bo parts GmbH, a tier one and tier two supplier to the automotive industry, is establishing a new facility in Greenville County, S.C. The $4.1 million project will create 100 new jobs.

In wake of Toyota-Mazda decision, Chatham County, N.C., approves options on megasites

Chatham County has approved five-year option agreements for both the Chatham-Siler City Advanced Manufacturing Site and the Moncure Megasite. Both sites are located in Chatham County and both meet the requirements for an automotive assembly facility.

Auto parts supplier expands in Tennessee

U.S. Tsubaki Automotive is investing $35.8 million to expand its facilities in Portland, Tenn. The parts supplier will also add 70 new jobs.

Auto parts maker to expand in Mississippi

Ohio-based S&A Industries announced it will invest $4 million to expand its plant in New Albany, Miss. The company, which will hire 40, makes noise vibration damping products for automakers.

Another megasite in the South tries to land Toyota-Mazda

The Purchase Area Regional Industrial Authority that covers several counties in Western Kentucky is offering up more than 2,000 acres of free land in an effort to land the latest automotive assembly plant site search in the Southern Auto Corridor. The site is in Graves County near Mayfield, Ky. According to sources, about 15 states in the South and the Midwest are competing for the proposed $1.6 billion plant that will build Toyota Corolla models and a Mazda SUV.

Automakers in Alabama shipped vehicles to 86 countries last year

Alabama’s automotive industry is in its 20th year. Last year, Hyundai, Honda and Mercedes-Benz shipped $7.9 billion in Alabama-made vehicles to 86 different countries. The number is a 13 percent increase over 2015 exports. Germany was the top export market for Alabama-made vehicles with more than $2.4 billion, followed by China, Canada, Mexico and the United Kingdom.

Florida-Alabama megasite makes pitch to Toyota-Mazda

In the Florida Panhandle, just South of the Alabama-Florida line and Dothan, Ala., lies the 2,240-acre Florida-Alabama Mega Site. The site is relatively new to the large number of megasites in the South. Alabama and Florida officials have contacted leaders of the Toyota-Mazda joint venture to build electric sedans and SUVs. The site is located 30 miles from Dothan, 49 miles from Panama City, Fla., and 63 miles from Tallahassee. The city of Marianna, Fla., operates a municipal airport 12 miles from the site.

For real-time news on business, politics and economic development in the South, go to www.RandleReport.com. For all projects announced in the South, go to www.SB-D.com. For more information on the automotive industry in the South, go to www.SouthernAutoCorridor.com.

Kentucky has become the center of aluminum manufacturing for the automotive industry

South Carolina automotive plant moving to Mexico

Who’s in the running for Toyota-Mazda plant?

Freightliner to open $27 million logistics center in North Carolina

Toyota Motor North America expands Plano, Texas operations hub

Sentury to build North American HQ and tire plant in Georgia

Parts supplier to establish new operation in South Carolina

In wake of Toyota-Mazda decision, Chatham County, N.C., approves options on megasites

Auto parts supplier expands in Tennessee

Auto parts maker to expand in Mississippi

Another megasite in the South tries to land Toyota-Mazda

Automakers in Alabama shipped vehicles to 86 countries last year

Florida-Alabama megasite makes pitch to Toyota-Mazda

For real-time news on business, politics and economic development in the South, go to www.RandleReport.com. For all projects announced in the South, go to www.SB-D.com. For more information on the automotive industry in the South, go to www.SouthernAutoCorridor.com.

European auto supplier to open first U.S. facility in Alabama

An automotive company based in Spain is investing $30 million in a new wheel assembly plant in Tuscaloosa County. Truck & Wheel Group’s move will create more than 70 jobs.

Bolta opens $49 million Alabama plant

Global auto parts supplier Bolta Group has opened its new $48.7 million production facility at the Tuscaloosa County Airport Industrial Park. The factory will add 350 to its current staff of 200. Bolta manufacturers parts such as nameplates and decorative trims for the automotive industry.

German logistics firm launches in Greer, S.C.

Rudolph Logistics Group is launching a new warehousing operation in Greer, bringing more than $18 million of capital investment to the Upstate and creating at least 150 new jobs. Its customers include Audi, BMW Group, Continental and Mercedes parent group, Daimler.

BMW facility to draw thousands to College Park, Ga.

BMW plans to open a training center in College Park next to the Georgia International Convention Center, moving the training out of its Southern region headquarters in Sandy Springs. Officials in College Park expect the training center will draw as many as 10,000 BMW workers annually for corporate training. At 53,000 square feet, the new $16.6 million center will be four times as big as the old one. It will mainly be used for interactive training of dealership employees.

Gateway Tire to invest $11 million in Alabama

Gateway Tire, a wholesale distributor of brands such as Toyo and Hankook, announced plans to invest $11 million to open a 200,000-square-foot tire distribution center in Dothan.

Shapiro Metals opens second Alabama plant

Shapiro Metals recently launched its 11th North American plant with the opening of a new 20,000-square-foot facility in Decatur, Ala. The plant recycles metals from aerospace, trailer manufacturing, automotive and medical device customers.

Calsonic Kansei undertakes major expansion at Mississippi plant

Japan-based automotive supplier Calsonic Kansei will invest $16.33 million to expand its manufacturing plant in Madison, Miss. The company plans to create 98 new jobs, bringing its total employment in the area to about 600. Calsonic Kansei is a supplier to Nissan’s Canton automotive assembly plant.

Netherlands-based manufacturer bringing 71 jobs to Spartanburg County

Netherlands-based AWL-Techniek, a producer of high-tech welding machines primarily for the automotive market, will invest $2.53 million to establish its first plant in the U.S. The project also means 71 new hires.

Auto supplier adding 98 jobs in Tennessee

Automotive supplier Cooper Standard will create approximately 98 new jobs at its facility in Surgoinsville. Alongside the new jobs, the company, which is headquartered in Michigan, is investing $1 million in new plant equipment.

Electro-Spec launching new operations in Lexington County, S.C.

Electro-Spec, a specialty plating manufacturer for the aerospace and auto industries among others, is locating new production operations in Lexington County. The development is projected to bring $3.1 million of capital investment and create 53 new jobs.

Honda supplier expanding and hiring in Alabama

A Canada-based automotive metal-forming company is planning another facility for its plant in Sylacauga, Ala. Fleetwood Metal Industries is building a 60,000-square-foot facility close to its current plant in Sylacauga’s industrial district, and plans to hire 70 more employees by year’s end.

Toyota opens the doors of its billion-dollar campus

About 2,000 team members are arriving at Toyota North America’s new 100-acre, 2.1 million-square-foot campus it expects to operate for the next 60 years.

Giti Tire building $560 million campus

Singapore-based Giti Tire, the 10th largest tire company in the world, is on track to open its first North American manufacturing and distribution facility on a 1,100-acre site, 170 miles northeast of Charleston, in Richburg, S.C. The company expects to invest $560 million and create 1,700 new jobs over the next decade in Chester County.

Automotive supplier to build in Charleston County, S.C.

Knapheide Manufacturing Co. announced recently it is opening a new manufacturing facility in Charleston County, expected to bring an investment of $1.3 million and create 63 jobs. The new plant will install van interiors and bodies for Mercedes-Benz

BMW commits to new jobs in U.S.

BMW AG is the latest auto maker to commit to new jobs at a U.S. factory following criticism from President Donald Trump, saying it will create 1,000 American jobs through 2021 as it works to boost its production of sport-utility vehicles in South Carolina. The jobs are part of a $600 million investment planned for the German auto maker’s Spartanburg factory.

By Michael Randle, EDITOR

Some are saying that North Carolina is the front-runner for Toyota and Mazda’s proposed $1.6 billion, 4,000-employee plant that the Japanese automakers are shopping around the U.S. The advantages are numerous for the Tar Heel State, sources say. They cite four excellent megasites in the state — two in Chatham County near the Research Triangle, one in Randolph County near Greensboro and another in Edgecombe County near Rocky Mount. North Carolina also has one of the largest workforces in the South in an age of very tight labor.

Also weighing in North Carolina’s favor, some sources say, is the fact that the state is not currently home to what we call a “Big Kahuna,” or a major automotive assembly plant. Plain and simple, automotive plants are the Big Kahuna in economic development. No projects have the economic effect that an automotive plant has on a state, multi-county region or a city. Simply put, they are the largest drivers of wages in the South. In 22 of the last 23 years, the automotive industry has led all sectors in the region — services or manufacturing — in large projects of 200 jobs or more.

Arkansas, Florida, Louisiana, North Carolina, Oklahoma and Virginia are the only states left in the South that are not home to at least one major automotive assembly plant. Louisiana and Oklahoma were home to GM plants, but those closed in the last 12 years.

Of those states void of a major automotive assembly plant, North Carolina and Virginia would be ranked No. 1 and No. 2 in the prospect of landing one in the Southern Automotive Corridor. After all, North Carolina was a finalist for the Toyota plant that ended up in Blue Springs, Miss., in 2007. The state was also a finalist for the Mercedes-Benz plant that announced in Alabama in 1993. In both cases, North Carolina was outbid badly by Mississippi and Alabama when it came to the incentive packages offered.

Just like those two projects, North Carolina will have to pony up for the Toyota and Mazda joint venture, unlike it has ever done for a large job generating deal. The largest incentive package I can recall that North Carolina has doled out over the last 25 years was to Dell when it opened a computer factory in Winston-Salem in 2005. That package totaled over $200 million. However, Dell didn’t even get a whiff of a large portion of that $200-plus million. The plant closed four years after opening and most of the incentives paid to Dell were returned to state and local agencies via claw back provisions.

North Carolina has written into its state budgets this year and next up to $50 million in incentives toward a “transformative” project. According to the provision, that amount could be offered by the state for a project of $4 billion in capital investment and a 5,000-employee commitment. Let me tell you, it’s going to take a lot more than $50 million to land this latest Big Kahuna. In fact, it might take $500 million to land the project, which will be the most efficient automotive factory in the world using artificial intelligence and connectivity to build automobiles. Toyota will most likely make electric Corolla models and Mazda will make electric SUVs at the proposed plant.

Other than the aforementioned sites in North Carolina, we’ve heard Toyota officials have already looked at the Glendale Megasite in Hardin County, Ky; the Huntsville Megasite in Limestone County, Ala.; and the Memphis Megasite in Haywood County, Tenn. It should be noted that in addition to Toyota’s plant in Mississippi, the automaker has an engine plant in Huntsville, Ala., and its largest U.S. plant in Georgetown, Ky. Again, in an age of very tight labor, let’s not forget there are thousands of out-of-work coal miners in Eastern Kentucky.

There have been nine new foreign-owned automotive plants built in the Southern Automotive Corridor since Mercedes announced it was building its Alabama plant in 1993. Right up to the day before that transformational Alabama project, The Wall Street Journal had picked a site in Mebane, N.C., as the site for the German automaker.

After decades of being the bridesmaid in auto assembly announcements, this Toyota-Mazda site search could actually end up in North Carolina. But I will believe it when I see North Carolina write the check for this latest Big Kahuna.

By Michael C. Randle

In a post-truth, alternative facts, fake news world, brought about almost exclusively by the far-left and far-right media, as well as political officials on the fringe, what are we supposed to believe? What we can trust is the data. So, let’s look at the data that busts some of the myths that are out there now in an effort to find the truth about the current economy.

Quarterly economic data from the federal government did not exist until after World War II. Therefore, it is difficult to trust sources prior to then when it comes to economic expansions or recessions.

Based on the data, an economic expansion is defined as a measure of economic growth from one quarter to another. It is essentially the rate of change in the nation’s gross domestic product. Some measure the growth or decline of an economy from one year to the next, but mostly, it is factored quarterly.

If GDP grows each quarter — the current economy has expanded for 31 consecutive quarters, or almost eight years — that is considered an expansion. A recession is defined by the federal government and economists as a decline in real GDP, income, employment, retail sales and manufacturing for at least two quarters, or six months. That has not occurred with the nation’s economy since the first and second quarters of 2009.

The current economic expansion is very impressive, but it is not the second-longest in U.S. history, or even the second-longest post-World War II. The nation’s economic expansion from the first quarter of 1961 to the fourth quarter of 1969 lasted 36 quarters, according to the U.S. Department of Commerce. That was the second-longest expansion in U.S. history.

The nation’s economy advanced by 32 consecutive quarters from 1982 to 1990, making it the third-longest expansion. And the expansion of the go-go 1990s from 1991 to 2001 lasted 38 quarters, or nine and a half years, the longest economic expansion ever recorded.

Regardless, this current economy is in rarefied air, and no one who has the data can call it a recession as we have heard from some far-right news sources. One more quarter of an advancing economy and we will have tied the third-longest expanded economy.

And the data says: The length of the current economic expansion is not the second-longest in U.S. history. It is the fourth-longest in the nation’s history (or since quarterly GDP numbers were first calculated in 1949).

Workforce participation rates are not great, they are average, which is really not the problem. The real problem is most who claim the quote above, or anything like it, don’t even know the definition of “workforce participation.”

“Workforce participation rate” is defined as the percentage of people from age 16 to 64 years old, either holding a job or actively seeking work. High school and college students who do not have a job are deemed “not participating.” Retirees in nursing homes are considered “not participating.” The disabled are considered “not participating.” Stay-at-home persons who can’t afford childcare or elder care are considered “not participating.” I’m sure there is a kid somewhere who is 16 years old, driving his Camaro to junior high because he failed the ninth grade twice. Yes, that kid is considered “not participating” in the workforce.

Also, the severely addicted, if not working or seeking a job, are considered “not participating,” as are the mentally ill, which should be addressed when discussing workforce participation, or lack thereof.

Arguably, one of the reasons the workforce participation rate is just average at 63 percent is that back in the 1990s when it was so high (67 percent), there were very few drug tests taken when applying for a job. Today, drug tests are almost mandatory due to insurance regulations.

Drug use is part of the reason many people don’t participate in the workforce. There is more illegal drug use in this country than ever before, which has been documented by many sources. That’s a big portion of the work-eligible, participation problem. What’s the point in applying for a job, when many think, “I won’t pass the drug test.”

There is no question that drug tests administered when applying for a job are keeping workers on the sidelines. So, it is a little unfair to compare workforce participation rates today to the days when drug tests were rarely if ever given.

Since 1970, the highest workforce participation rate was in March 2000 at 67.3 percent of eligible workers with a job or seeking one. Today, the workforce participation rate is right at 63 percent. For the year 1970, the labor participation rate was 60.4 percent. At no time since has it ever risen above 67.3 percent.

And the data says: At 63 percent, workforce participation rates today are not the worst in U.S. history. Since 1970, we’ve seen workforce participation rates drop to 60.4 percent, and the highest ever was 67.3 percent. So, workforce participation rates today are a little below average the rates seen since 1970.

It should also be noted that over the last 18 months, the civilian labor force climbed nearly 2 percent, a very strong pace. That growth came from workers reentering the workforce. And the prime-age workforce participation rate (ages 25 to 54 years) has surged to 82 percent, the highest in nearly three years.

Since 1960, annual wage growth or decline has bounced from its highest at 13.77 percent to a low of minus 5.77 percent. In recent recoveries like the one we are in now, wages on average grew by about 3.7 percent per year. According to the Bureau of Labor Statistics, wage growth in the U.S. averaged 6.29 percent from 1960 to 2016. But that average counted many years in the 1960s of fast-rising wages, and in the 1970s of spiking inflation.

In the last three decades, wages have not come close to growing by the 6.29 percent annual average, particularly post-Great Recession. In fact, average hourly wages grew by only 2.9 percent in 2016, and that was one of the best years in a decade. Wages grew by 2.3 percent in 2015, and 2.1 percent in 2014. If hourly wages had grown by 3.7 percent in 2016, the average during recoveries, workers would be making nearly $30 an hour compared to the $26 average today.

However, in former President Obama’s defense regarding his claim, the median household income grew to $56,500 in 2015 (adjusted for inflation), according to the U.S. Census Bureau. That’s growth of more than 5 percent in real median household income.

That 5 percent gain is the largest annual increase in income since median household income data has been recorded, which began in 1968. . .which is probably what Obama was referring to.

And the data says: Wages have not grown faster over the past few years than at any time in the past 40 years. President Obama was wrong.

Under President Obama’s watch, at least 2 million jobs were created in each of his last six years in office. During that time, the U.S. set a record for the most consecutive months of creating 200,000 jobs or more. Under Obama, the U.S. created 2.2 million new jobs in 2016 and 2.7 million in 2015.

On the other hand, Obama’s administration claimed that more than 15 million jobs were created in that administration. That’s a gross figure, which they failed to point out. Remember, the Obama administration began in January 2009. At that time and until 2010 (the first full year of recovery), the U.S. was bleeding hundreds of thousands of jobs monthly. That being the case, Obama’s net job creation total was 11.3 million jobs.

That total was still much better than President George W. Bush’s two terms, which saw only 2.3 million net new jobs created. But Obama’s net jobs figure did not compare to Ronald Reagan’s two terms (15.9 million net jobs) or Bill Clinton’s two terms (22.9 million net jobs).

And the data says: True, the 77 consecutive months of job growth in the U.S. under the Obama and Trump administrations is indeed a modern-day record.

In the recent presidential election, Donald Trump said in the final debate, “We don’t make our product anymore. It’s very sad.” He then said, “We’ve given up.”

We did give up in the 1990s, when those comments by President Trump would have been applicable. Back then we simply could not compete in the manufacturing arena with China. Today, we compete very favorably with every country in the world, including China and Mexico, for new and expanded manufacturing industries.

In an article published by CNN Money in the fall 2016 quarter, Chad Moutray, chief economist with the National Association of Manufacturers, was quoted saying, “We produce more today than we ever have. We made $2.1 trillion worth of products in 2015.” In fact, in the first quarter of 2016, the value of products made in America reached a record high. Which means that we are experiencing the most productive period in manufacturing history in this country.

Today, U.S.-based factories — both foreign-owned and domestic — are making almost five times more product than in the 1950s and ’60s, and they are doing it with many less workers. That’s where people can get confused about the manufacturing sector and its performance in the U.S. The job losses are important, but misleading.

In 1979, manufacturing employment peaked at 19.6 million workers. Today that figure is about 12.4 million and it has stabilized. In fact, over the last six years, the U.S. has created net new manufacturing jobs for the first time in more than two decades. Since the end of the recession, the U.S. manufacturing sector has added more than 800,000 jobs, with about 40 percent of those in the South. And compared to 1960 when one in four Americans had a job in manufacturing, today only one in 10 work in the sector.

The best way to understand advanced manufacturing today is to look at the history of the farm workforce in the U.S. In 1880, roughly 50 percent of Americans worked on a farm. Today, that figure is below 2 percent. The reason is the same reason jobs have been lost in the manufacturing sector; automation on the farm and on the factory floor have reduced both workforces.

And the data says: In the first quarter of 2016, the value of products made in America reached a record high. Today, U.S.-based factories — both foreign-owned and domestic — are making almost five times more product than in the 1950s and ’60s. The real issue is that the nation’s manufacturing sector is making more today than ever with about 60 percent of the peak manufacturing workforce of 1979. Yes, we have lost millions of manufacturing jobs, primarily to automation, but President Trump is wrong. The U.S. manufacturing sector makes more products than ever.

When campaigning for the Democratic nomination for president, Sen. Bernie Sanders introduced a bill that would raise the federal minimum wage to $15 an hour. This is not a black-and-white argument that can be fact checked like the previous statements simply because the minimum federal wage hasn’t been raised to $15 an hour, or even to $8 an hour, so it’s impossible to make a definitive statement on right or wrong based on its effect on the economy. It is more of a gray area that needs to be discussed among unbiased, nonpartisan minds.

There isn’t any question that Sanders is right when he said “the federal minimum wage” of $7.25 an hour is “a starvation wage.” You would have to be far right of the Tea Party if you believe that $7.25 an hour is a fair wage. It hasn’t increased since July 2009. There is no question that it needs to be raised. However, an across-the-board advancement of the federal minimum wage from $7.25 to $15 an hour would make some areas of the nation incredibly vulnerable, and place those areas in noncompetitive positions.

Wages are the most important aspect of any economy in my opinion. When it comes to the practice of economic development, wages are the only thing the vast majority of people — outside of economic developers and economists — truly understand. The economic development community tries to explain to elected officials, business leaders, local and statewide media as well as the citizenry at large, why a job-generating project is so important to a community and why incentives to capture that project are so critical. But they do a very poor job in their explanations.

In an age of “corporate welfare” accusations when it comes to incentives, simplifying the return on investment of a job generating project can be very effective. At the moment I am writing this article, some politicos in Florida want to abolish Enterprise Florida, the only statewide economic organization in the state. It has come to this because the economic development community in the state cannot seem to argue the merits of Enterprise Florida and the incentives the organization hands out to new and expanding business and industry.

Again, few people outside of it understand the practice of economic development — tax generation, multipliers and revenue streams that come from a job- and investment-generating project. And if an elected official’s proposed incentive is based on tax generation, then those outside of economic development would simply say to themselves, “I don’t trust them with that money, either.”

However, wages are something that everyone understands, because most everyone earns a wage. Wages go directly to the people and not first to the government. I often tell people who are charged with explaining how economic development works to focus on the wages a single project will inject into a community.

For example, the BMW plant in South Carolina generates about $700 million in wages for the Upstate region each year, not including the automaker’s suppliers. Count suppliers, and the wages are upwards of $1.7 billion a year for a single project. The plant has been operating since 1994, and it will continue to roll out SUVs for many years to come, meaning the incentives paid to BMW are a pittance compared to the wages generated over the course of, say, the 75-year lifespan of the plant.

I remember when a far-right think tank from North Carolina accused me in 2003 of being a fiscal liberal because of my support of incentives. I told the far-right editor who was interviewing me that Alabama has spent less than $2 billion in incentives to three automotive assembly plants — Mercedes-Benz, Honda and Hyundai — since 1993. The wages paid at just those three assembly plants are today right at $20 billion dollars. Those wages don’t count the hundreds of suppliers the three facilities have drawn to Alabama. So far, Alabama has enjoyed more than ten times its return on investment in wages alone!

The editor of the far-right think tank would have none of it. He said, “I think all ‘corporate welfare’ should be directed to education and public safety.” I said to him, “Well, if you do that, North Carolina will be the safest, smartest, 20 percent unemployment state in the South.”

But back to Bernie Sanders and his recent quest to advance the federal minimum wage to $15 an hour all across America. I think everyone would support higher wages for all if, of course, it didn’t come at the expense of someone else’s pocketbook. Obviously, that is not possible.

A $15 wage increase across the nation is ludicrous. Sanders wanted to raise the federal minimum wage the same amount for New York City, San Francisco and Los Angeles as with Martinsville, Va., Monroeville, Ala., and Alexandria, La? That makes absolutely no sense.

If you raised the minimum wage in those last three areas to $15 an hour, they couldn’t compete, and while not all three are considered “rural,” the rural South and much of rural America would immediately lose any competitiveness they now have because the wages would be too high for employers. The rural South is competitive for cost reasons and natural resource-based reasons only in today’s economy. Take out the cost advantage from the rural South and they are out of the game, forever.

It doesn’t make sense to me to have a universal hike in the minimum wage for all states or cities. For example, the minimum wage in New York City is $11 an hour. But that $11 only has the purchasing power of $7.36. Here in Birmingham, Ala., the minimum wage is $7.25, but it has the purchasing power of $8.06.

MIT’s Living Wage Calculator exemplifies the differences in earning thresholds and cost of living indexes from around the country. The Living Wage Calculator provides “cost-adjusted estimates of what workers and their families need to make in order to support a basic living in the communities in which they reside.” The developer of the MIT Living Wage Calculator, Dr. Amy Glasmeier, defines a living wage as “the wage needed to cover basic family expenses plus all relevant taxes.”

By using the Living Wage Calculator, you can determine what you need to make for a living wage in every county in the country. In San Francisco County, Calif., it’s $14.37 an hour to achieve a basic living for one adult. The minimum wage in California is $10.50 an hour.

Third Way, described by The Wall Street Journal as a “center-left think tank” and by The New York Times as “radical centrists” and “incorrigible pragmatists,” has taken MIT’s Living Wage Calculator further. Third Way proposes establishing five different minimum wage hikes based on the cost of living in metros. Third Way calls their plan “a regional minimum wage.”

Third Way policy adviser Joon Suh writes on the think tank’s website and in the story titled, “Doing the Right Thing, the Right Way: A Regional Minimum Wage,” what he believes is a fair way to go about raising the minimum wage.

Third Way proposes to replace the single federal minimum wage with a regional minimum wage with readjustments every three years. The think tank believes that the new wage would range from $9.30 per hour in low cost regions to $11.90 per hour in high cost areas. That would set the median federal minimum wage at $10.60 per hour, about where the political centrists believe it should be.

It’s my view that five regional federal minimum wage floors are not enough. Some small manufacturers in rural areas of the South would get hammered by a $2-an-hour hike in the minimum wage, particularly in areas like the Mississippi River Delta and Appalachia.

And the data says: As written, one cannot form a black-and-white, data-centric answer to raising the federal minimum wage. Yet, using MIT’s Living Wage Calculator to set the federal minimum wage is certainly a start to one of the most important aspects of our economy.

Both Treasury Secretary Steven Mnuchin and President Donald Trump think the Bureau of Labor Statistics cooks the books when it comes to the monthly unemployment report it publishes each month. Both men totally refuse to believe that the nation’s unemployment rate is 4.7 percent. With 95 million Americans over the age of 15 without a job or not looking for one, surely the unemployment rate cannot be as low as 4.7 percent. There are only 325.5 million people in the country.

As mentioned in the workforce participation section of this story, those outside the labor force can be current high school and college students, stay-at-home parents, prisoners, the disabled and retirees. At a workforce participation rate of 63 percent today, down from 66 percent prior to the Great Recession, the U.S. labor force is the smallest it’s been since the 1970s when the participation rate was as low as 60 percent.

Is the 63 percent workforce participation rate a sign of a weak economy and fewer available jobs, or are demographic factors such as retiring baby boomers to blame? To answer that, let’s look at current statistics. There have been over 5 million jobs available in this country for years. If there is a large block of available labor out there, why aren’t those jobs being filled?

Companies large and small are having a tough time filling positions, many times because the skills needed for those positions can’t be found in the labor shed. Again, if there are so many people in this country who can’t find jobs, then why are 5 million jobs seemingly always available to those people?

There are many announced job-generating projects on hold this very minute because labor is not available in certain areas of the South. For example, several large petrochemical plants in Louisiana and Texas are being delayed because of a lack of construction labor. These projects are waiting on other companies to finish a project, freeing up labor. Construction jobs are considered temporary, but not in the petrochemical industry in Louisiana and Texas. Welders, for instance, will finish up at one plant then start on a new project that may have been delayed for up to a year because there was no available labor, or specifically, no available welders.

Let’s see what driving up the workforce participation rate would do for labor in this country. At no time since 1970 has there been a workforce participation rate that was higher than 67.3 percent. That high mark was set in 2000. Today’s rate is 63 percent, so a difference of 4.3 percent. So, if we met the highest workforce participation rate seen since 1970 today, that would mean an additional 4.4 million workers. That’s not many, and wouldn’t even fill the 5.5 million available jobs that are out there now.

The fact is, since 1970, there has always been between 33 to 40 percent of the workforce over 15 years of age that does not work or does not look for work. So the facts point really to demographics. The sad truth is, this nation is getting older and its population growth is the lowest it has been since the Great Depression.

There is still some slack in the labor market, but it isn’t nearly what President Trump and Treasury Sec. Steven Mnuchin believe. The fact that there were 235,000 jobs created in February proves there is still labor slack. It was interesting that President Trump, who has said that the monthly Bureau of Labor Statistics jobs report is “one of the biggest hoaxes in American politics,” took credit for the great February jobs report. He also said about the February jobs report, the first while in office, “I think it’s going to continue big league.”

So, yes, the demographics indicate that this year and next we could still see some months of 200,000-plus job gains, but those months are dwindling. With a 4.7 percent unemployment rate, we are nearing full employment and that has been supported by the Federal Reserve. Add that to the fact that this administration could deport millions of undocumented people and slow immigration, we could soon be in a situation where we have a shortage of unskilled labor, not just skilled labor.

But all of that pales in comparison to these demographic figures. . .as written, this nation is aging, but at the same time, the U.S. fertility rate fell last year to its lowest rate since the government began keeping track in 1909. The general fertility rate is the average number of births from 1,000 women ages 15 to 44 years old. In 2016, the fertility rate dropped to 59.8 births per 1,000 women, the lowest ever. In addition to the lowest fertility rate in more than 100 years, the U.S. saw the death rate rise last year for the first time in a decade. According to the Census, the U.S. population in 2016 grew at its lowest rate (0.7 percent) since 1936-1937.

Yes, the demographics have our backs against the wall when it comes to the current and future labor force. Of course, the wild card is how many jobs over the next decade or even longer will be replaced by automation. If it is in the millions, the current and future labor shortage will take care of itself.

In the meantime, not factoring in job losses to automation (because I am not sure anyone can put a finger on that number at this point), the labor force is shrinking and fast. The fact of the matter is the growth of the working age population (between 16 and 65) is slowing dramatically. Demographic math is cutting into our available workforce.

For example, from the 1970s to the 1990s, the economists’ standard for job growth in this country was 150,000 jobs created per month. Above 150,000 jobs created per month and the jobless rate would drop, and anything below 150,000 jobs created per month caused the jobless rate to go up.

From the 1970s to the late 1990s, the working age group of 16 to 64 years was growing on average nationally of about 200,000 people a month. The working age population rose by just 71,000 per month over the past two years. And the Census Bureau reported in the fall quarter that the working age population will grow by an average of just 50,000 per month over the next 15 years, which is alarming.

So, 20 years ago, 200,000 people became work eligible each month, but now only 71,000 per month become work eligible in this country. That does not mean the economy is doing poorly. It just means we are seeing less and less people enter employment age.

Today, you can throw away that standard number of needing to create 150,000 new jobs per month. To absorb the current slower growing population, we only need to create about 50,000 jobs per month to sustain a healthy economy. And in a few years, that will drop to 33,000 new jobs per month.

President Trump has set some big goals for the economy. He has promised to create 25 million jobs over 10 years. That’s more than double what has been created under Obama and more than Ronald Reagan or Bill Clinton’s terms. But where will that labor come from? It apparently won’t come from immigrants, and if he deports large numbers of people living in this country, we will see reductions in an already tight labor market.

And the data says: There will always be anywhere from 33 to 40 percent of the workforce that is not participating, unless governments end social, poverty and disability assistance. The U3 unemployment rate is 4.7 percent and the U6 is 9.4 percent. There is no measure that we can find that indicates the true unemployment rate is 20 percent or higher. If anything, we are at or near full employment. And the demographics indicate clearly that the number of people entering the labor force will be at historic lows for many years to come.

The demographics also indicate that creating 25 million jobs over the next 10 years is simply impossible, given the lack of growth in our population. The only way to enlarge the labor force over the next decade or so would be to increase immigration from the current 1 million a year to around 3 million a year, and that is not going to happen. Or, perhaps automation could free up millions of needed workers, but that remains to be seen.

By Michael Randle

There’s a lot of talk right now about trade agreements. Not all of the usual suspects are in support of two proposed free trade agreements in this political cycle. Some blame NAFTA and free trade in general as elements that have reduced the middle class in the U.S., while building the middle class in Mexico and elsewhere. Yet, in 2015, almost 50 percent of U.S. exports went to the 20 countries the U.S. currently has free trade agreements with. Those countries do not include any in Europe, nor do they include China or Japan.

We do have free trade agreements with Australia, South Korea, Israel, Singapore, several countries in Central and South America, and, of course, Mexico and Canada. With the FTA countries, the U.S. enjoyed a trade surplus in manufactured goods of about $12 billion last year. Not so much with those we do not have trade agreements with. . .regarding those countries, we have a trade deficit of about $500 billion.

There are two major trade agreements that are currently proposed. One is with the European Union and the United States, trading partners that accounted for about one-third of U.S. exports last year. Called the Transatlantic Trade and Investment Partnership (TTIP), it is a companion agreement with the Trans-Pacific Partnership (TPP). That agreement involves 12 countries: the U.S., Japan, Malaysia, Vietnam, Singapore, Brunei, Australia, New Zealand, Canada, Mexico, Chile and Peru. The pact is designed to create stronger economic relations between the member nations, cutting tariffs and fostering trade to boost growth in exports and imports.

I will not take sides on the free trade agreement argument. It is a complicated issue. I can clearly see the basis of the arguments for and against these trade agreements. But I do know this: the Southern Automotive Corridor has lost out on nine major automotive assembly plants in the last few years to Mexico, primarily because Mexico has free trade agreements with more than 40 different countries. That’s more than double the number of countries the U.S. has trade agreements with, and that alone is a major factor for manufacturers when it comes to exporting.

Exports fall for the first time since the recession

For the first time since the end of the recession, the total value of U.S.-exported goods fell from one year to the next. In 2015, the U.S. exported about $1.5 trillion in goods, including high value products such as automobiles, aircraft, machinery, telecommunications and chemicals, among other goods. That was down about 7.5 percent from 2014 when the U.S. exported $1.63 trillion in products, but well above the $1 trillion exported in 2006 prior to the recession. The $1.63 trillion in goods exports in 2014 was the largest total ever for the U.S.

The South also saw a reduction in the value of its exports in 2015 from its record year of $654 billion in 2014. The South exported $61.7 billion less in 2015 than in 2014.

One of the reasons for the drop in exports can be attributed to the resilient U.S. economy. With a strong economy comes a stronger currency. Exports have tumbled in part because of the strong dollar that’s made American-made goods and services more expensive. Put that on top of a weak global economy and it’s not a mystery why exports fell last year.

Last year, the U.S. was the second largest exporter in the world, behind only China. China exported $2.27 trillion in goods in 2015. Germany was third with $1.3 trillion, followed by Japan with $625 billion. The American South’s total value of $593 billion exported in calendar year 2015 would make it the fifth largest exporter in the world if it were a country.

The 15 states that make up the American South led the other three U.S. regions by a wide margin in export values (see pages 46-47). In fact, the South accounted for 40 percent of U.S. exports last year. If worldwide demand increases this year and next, the region is positioned to set export records because of the increased manufacturing capacity of high value products that have come on line in the last three years or are currently under construction.

For example, all but one of the 17 major automotive assembly plants in the Southern Automotive Corridor have expanded since the end of the recession, three more than twice. And two major automotive assembly plants were announced last year — Volvo and Daimler Vans in South Carolina — that have yet to begin production. Both plants are designed to export at least half of their yearly vehicle production totals.

Furthermore, the fracking frenzy has expanded chemical production in Louisiana and Texas at a furious pace. Additionally, multi-billion dollar LNG export facilities are coming online in Louisiana and Texas, with the first — Cheniere Energy in Southwest Louisiana — already exporting the essential and abundant energy product. New aircraft, spacecraft, engine and rocket production are coming online, and the South is now home to two of the nation’s three large commercial aircraft assembly facilities with Airbus in Mobile, Ala., and Boeing in North Charleston, S.C. The other is Boeing’s massive Puget Sound facility in Washington State.

Job generation tied directly to exporting is growing as well. In 2014 (latest figures available) almost 2.9 million direct jobs were tied to exporting in the 15-state American South. With dozens of inland and deep-water ports — more so than any other U.S. region — the South is set up perfectly for companies that want to expand export capacity.

The rise of the middle class in the South?

In this presidential campaign, a lot has been said of the 40-year decline of the middle class. There is no question the middle class is weaker financially than at any point in the last three generations. Some estimate that prior to the recession, jobs that paid $60,000 were replaced by jobs that pay $40,000. Wage earnings have flattened since the recession ended, even though they are perking up a little as most places in the South have reached, or are near, full employment.

There is also no question that during one of the longest economic expansions in U.S. history, those wages should be higher than they are currently. The stagnant wages are one of just a small number of negatives currently involving the U.S. economy. Otherwise, the data is off the charts, including more large projects announced in the South in 2015 than any year since this publication began counting in 1993.

Look, the executives of companies setting records for new and expanding projects in the South in 2015 are not stupid. If they saw a recession looming, or a challenged economy like you hear about constantly in this presidential election, those same executives wouldn’t have invested a record $90.5 billion in this year’s SB&D 100. Most of those investments won’t even come online for one or two years.

The Great Recession, along with new automation technologies that are taking boots off the factory floor by the tens of thousands, and offshoring manufacturing capacity to China, Mexico and elsewhere from the 1990s to the beginning of the recession have devastated the middle class in this country. Yet, one of the major reasons why the American middle class has been reduced in number may be what helps bring it back.

There is a new middle class that is greatly assisting the world economy right now, one that didn’t even exist 30 years ago. And it’s not the middle class of America. There are now more middle class Chinese than there are people in the United States. The Chinese middle class is growing faster than any economic demographic in the world, and they are demanding the purchase of foreign-made products, particularly from the U.S.

In an article published this summer by Businessinsider.com titled “Chinese imports of U.S. goods are about to soar,” writer Andrew Meola insists that 15 percent of the Chinese population will buy products from a foreign country this year, amounting to more than $85 billion in sales. He forecasts that the number of foreign goods purchased by the Chinese will rise to $157 billion by 2020. And according to a Boston Consulting Group (BCG) study, more than 60 percent of Chinese consumers said they would pay more for products made in the U.S. instead of in China. BCG also published a press release in the summer claiming that three-quarters of Chinese consumers plan to maintain or increase spending this year.

So, clearly, the economic dynamics of China are changing. Just a few years ago, there was no middle class in China. Now, it dominates Asia’s economy and prefers American products. This big new customer might just contribute greatly to a renewed and stronger middle class in this country.

The fact that more jobs are returning to the U.S. from China than are going there is also a relatively new phenomenon. Combined with the fact that the Chinese are investing in the U.S. in record numbers, it looks as if China will be bolstering the U.S. economy for years to come. These big changes in how China helps this country’s economy, instead of taking from it, will boost exports to levels never before seen in the U.S.

Foreign Direct Investment

The ebb and flow of goods and money from one country to another is the very essence of the global economy. Last year, there was a record $1.76 trillion in foreign direct investment flows around the world, according to the United Nations. Of that total, there were $721 billion in massive cross-border mergers and acquisitions. Some of those mergers and acquisitions included Merck KGaA’s $17 billion purchase of Sigma-Aldrich and GlaxoSmithKline’s $16 billion purchase of Novartis.

While FDI worldwide set a record, a record was also set in the United States. Expenditures by foreign direct investors rose to $420.7 billion in calendar year 2015, an increase of 68 percent from 2014. These investments by foreign entities included acquisitions, existing industry expansions and new greenfield operations.

Of the $421 billion invested in the U.S. last year, more than half, or $281 billion, was manufacturing related, including new, expanded and acquisition. Within manufacturing, large investments were seen in chemicals, automotive, consumer products, pharmaceuticals and medicines, among other sectors.

Some of the most active foreign investors in the U.S. in 2015 were the typical customers — United Kingdom, Japan, South Korea, Luxembourg, The Netherlands, Ireland, Canada, Switzerland, Germany and France. Again, it should be noted that China continues to invest in the U.S. at rates never before seen.

In 2010, China invested just $4.6 billion in the U.S. In 2015, China invested $15.3 billion in 171 U.S. projects according to the Rhodium Group. In the first two quarters of 2016, China has turned 70 deals for a total of $18 billion invested. One of those deals was China-based Haier’s acquisition of GE Appliances and its massive Appliance Park facilities in Louisville, Ky. China’s largest and most active investments the last couple of years have been in automotive, consumer products, information technology, communications technology and real estate.

Until recently, the Chinese have been no-shows when it came to investing in the South, and in North America as a whole for that matter. On average, from 2000 to 2009, Chinese companies invested about $1.7 billion a year in the U.S. That’s the total investment of one small petrochemical plant in Louisiana or Texas today. Strictly speaking, Chinese investment in the U.S. has been chump change. . .until recently.

So, really, for the first time in history, China is playing a direct role in the U.S. economy from a job- and investment-generating position. The number of Chinese-owned companies now operating in the United States at the end of the second quarter of this year is estimated to be about 1,800. Those companies are employing approximately 110,000 people. Employment in China-owned companies, according to Stephen A. Orlins, President of the National Committee on United States-China Relations, is expected to quadruple over the next five years. Five years ago, Chinese-affiliated companies employed just 15,000 workers in the U.S.

Some believe that the recent surge in outbound FDI from China is an indication of capital flight. China’s economy the last couple of years has been somewhat chaotic. Because of that volatility, Chinese investors could be stashing away capital in what they believe is a safe economic haven in the U.S. But according to the Rhodium Group, a firm that tracks Chinese investment in the U.S., more than 80 percent of all Chinese FDI transactions in the U.S. in the first half of this year “. . .falls into the category of strategic investment.”

We believe this surge in outbound FDI from China to the U.S. is simpler than capital flight or strategic investments. There is no question that reshoring, onshoring, nearshoring, make it where you sell it — whatever you want to call this economic shift in manufacturing capacity — is driving this Chinese investment run in the South and in the U.S.

For example, if it is getting more difficult to make a profit in manufacturing many products in China for U.S. consumption, wouldn’t it make sense for Chinese manufacturers to offshore production to North America? Also, if it is getting more expensive to manufacture in China, where does that leave Chinese manufacturers? It puts them in the same position as other companies that are reshoring to the U.S. The Chinese are offshoring to the U.S. for economic reasons simply because soon, a manufacturer will be unable to make a profit making something in China for U.S. consumption.

One example of the “make it where you sell it” phenomenon is the proliferation of foreign-made tire facilities announced in the South in recent years. If you could make tires in Asia for U.S. consumption and make a profit, that’s what Yokohama, Hankook, Kumho, Bridgestone and Giti — just five of the many foreign tire plants announced in the South in recent years — would do. Instead, those companies are finding it more profitable to produce tires here. In fact, at deadline, Chinese tire maker Sentury Tire Americas chose a site near LaGrange, Ga., for a $500 million greenfield plant that will house 600 workers.

Again, the $18 billion in Chinese investment in the United States in the first two quarters of this year represents the best “year” ever. But it doesn’t even remotely tell the whole story. According to Rhodium Group, the value of announced but not completed Chinese investments in the U.S. was near an all-time high of $33 billion at the end of the second quarter.

Some of the pending Chinese merger and acquisition deals out there currently include HNA Group’s $6 billion purchase for Ingram Micro, Anbang’s $6.5 billion acquisition of Strategic Hotels and Apex Technology’s $3.6 billion purchase of Lexington, Ky.-based Lexmark.

In the U.S., there are about $10 billion Chinese greenfield projects that are pending and have not been counted as investments by the end of the second quarter. In the South, those include Sun Paper’s $1.3 billion mill in Arkadelphia, Ark., China Jushi’s $300 million fiberglass plant in Richland County, S.C., and Yangfeng Automotive Interiors’ $71 million plant in Laurens, S.C., and its $55 million plant in Chattanooga, Tenn.

The large increase in FDI in the U.S. in 2015 is a sure sign that foreign investors view the nation’s economy as one of the safest in what currently is a chaotic world economic marketplace. And why not? For the most part, the nation is at full employment for the first time in 16 years, the stock market is humming and on a cost basis, the U.S. — particularly the South — is very competitive right now with just about any country in the world.

Regarding the current economic conditions in the U.S., Forbes publisher Rich Karlgaard wrote this summer, “Dismal though the political mood is today, the U.S. is heading into a remarkable era. The hand of cards America holds is like a royal flush: reliably cheap energy costs; low (on a global scale) real estate costs, especially in the South and Midwest; political stability; military strength; a growing population; the world’s best research universities; and global leadership in all the key digital technologies.”

To conclude, trade, exports and foreign direct investment are looking pretty good today, especially in the South. Other than wages that are stubbornly low, there are not many negatives regarding the U.S. or the South’s economy. Surely, now that the region is at or near full employment, wages must rise, right? Let’s get this presidential election out of the way, which can’t be assisting the economy, and I believe we will find out.

By Michael Randle

We are still in the second longest economic recovery period ever in this country, approaching 90 months. On top of that, at 74 months, the U.S. is enjoying what is now the longest stretch of consecutive monthly job creation on record. The recovery has been solid, with about 15 million jobs created, and 11 million of those new jobs. In September, we reached a record low level of layoffs and discharges of 1 percent according to the Bureau of Labor Statistics. Yes, workers are finally winning in this economy.

During this current recovery, the U.S. set a record for the most consecutive months of 200,000 or more new jobs created. Since January 2013, almost 9.7 million jobs have been created, averaging 224,000 new jobs each month. And all of this has been done in a time when the public sector hasn’t created jobs at all. From 2010 to 2013, the private sector added about 6.7 million jobs, while the public sector lost around 626,000, which is unprecedented. During President Obama’s two terms, the public sector saw a loss of 341,000 jobs.

The public sector is typically a huge job generator, especially at the federal level. However, because austerity practices have been implemented in an effort to stop adding to the national debt, lawmakers have slowed the hiring of government jobs. Many states aren’t hiring as well.

Some argue that the recovery from the Great Recession has been slow. Well, it wasn’t called the Great Recession for nothing. It should have been called the Great Crater or the Great Abyss. Long-term unemployment rose to historic highs during and after the recession, and the unemployment rate spiked almost to its post-war high.

The recessions in the early ’80s, ’90s or the one in 2001-2002 cannot even remotely be compared to the recession of 2007-2009.

The reason the climb from the crater has taken longer to get to pre-recession peaks is because the low point of the Great Recession was so low. The U.S. is at pre-recession unemployment lows now, at 4.6 percent, but it took 51 months to get there, according to the Economic Policy Institute. In comparison, the recession of the early 1980s took 11 months to reach pre-recession peaks, and the recession in the early 1990s took 23 months.

Yet, today, from an economic development perspective — at least here in the South — project activity is better than any time since this magazine began charting that activity in 1992. There were 730 projects meeting or exceeding 200 jobs and/or $30 million in investment in 2015, and 668 in 2014, both records. The last time you saw a year like that was in 1997 when 636 projects meeting or exceeding our thresholds were announced in the South.

As for corporate investment, some say it is declining. In fact, it is leveling off. The truth is that in Quarter 3 of 2015, a record $2.217 trillion was invested by private corporations in the U.S., according to Commerce. In Quarter 3 2016, that investment fell to $2.19 trillion, which is not far off the record set last year. So, corporate investment has stabilized near record totals.

Furthermore, in 2015, the largest 100 projects in the South had a total investment of $90.5 billion, easily breaking the then 23-year record set in 2014 of $78.2 billion. My question is, how can business investment be off when billions are being spent on new and expanded petrochemical plants in Texas, Louisiana and elsewhere? We are in the midst of the largest build-out of chemical plants since World War II.

The hundreds of massive petrochemical plants that have expanded or been built — or are under construction now — are the result of widespread fracking that began in the U.S. in the late 2000s. On average, the cost of natural gas to run a petrochemical plant in much of the U.S. is a third of costs in Europe, and even lower compared to Asia.

Furthermore, spending by the automotive industry — the second-most investment intensive sector aside from petrochemicals — has also been remarkable over the last few years in the Midwest and South. With the exception of one, every major automotive assembly plant in the South has seen automakers spending hundreds of millions, if not billions, on expansions since the recession ended. There is no question that the petrochemical and automotive industries led the South out of the recession.

In short, we have seen a remarkable climb out of the crater called the Great Recession, and it continues today. But, I hate to tell y’all this: The U.S. economy and the South’s economy are about to slow down, maybe noticeably, if there are pulls on the economy outside of labor. . .inflation for instance. And it’s not because of a new administration.

What is happening, without question, is that we are running out of labor, this country’s most prized economic asset. Sure, there is still some slack in the labor market, and there are millions of workers in the U.S. who can’t find a job, can’t find the right job, or are unwillingly working part-time. However, the long party of job generation of 200,000 or more each month may be over. . .and that’s not such a bad thing.

WORKER PARTICIPATION

Before I make my case that we are running out of labor, let’s address the issue that centers on the 35 percent of workers who are not participating in the workforce, yet are eligible, according to the government. Politically, this is a hot-button issue. If you are the voting block that doesn’t think the current economy is so great, you point to the labor participation rate. There is nothing wrong with that, but the fact is, there are 5.5 million jobs in this country that are available almost on a daily basis. There are more than 1 million jobs that remain unfilled in the tech sector. The jobs are there, the takers aren’t. Why?

In addition, some claim the current 62.9 percent labor force participation rate is far and away the lowest in the nation’s history. Nothing could be further from the truth. In 1970, the labor participation rate was 60.4 percent. At no time since has it ever risen above 67.1 percent.

It should also be noted that over the last year, the civilian labor force climbed nearly 2 percent, a very strong pace. That growth came from workers reentering the workforce. And the prime-age (25 to 54 years) participation rate has surged to 81.5 percent, the highest in nearly three years.

There are all kinds of reasons why people don’t seek work. Some are lazy, some are crazy, or both. Many are disabled. Some are recently retired but are still being counted as work eligible. Thousands join the military every year or go to prison and are still counted as work eligible. And millions more are currently in high school or in college and are counted as outside the labor force, or not participating.

Many don’t want to work and would rather take their legal and rightful federal assistance. If you are a single mother of four, say, and can’t find a job that pays as much as what you get from available federal programs that address poverty, who wouldn’t take what is legally available to them?